- 42.00 KB

- 2022-04-29 14:21:07 发布

- 1、本文档共5页,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,可选择认领,认领后既往收益都归您。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细先通过免费阅读内容等途径辨别内容交易风险。如存在严重挂羊头卖狗肉之情形,可联系本站下载客服投诉处理。

- 文档侵权举报电话:19940600175。

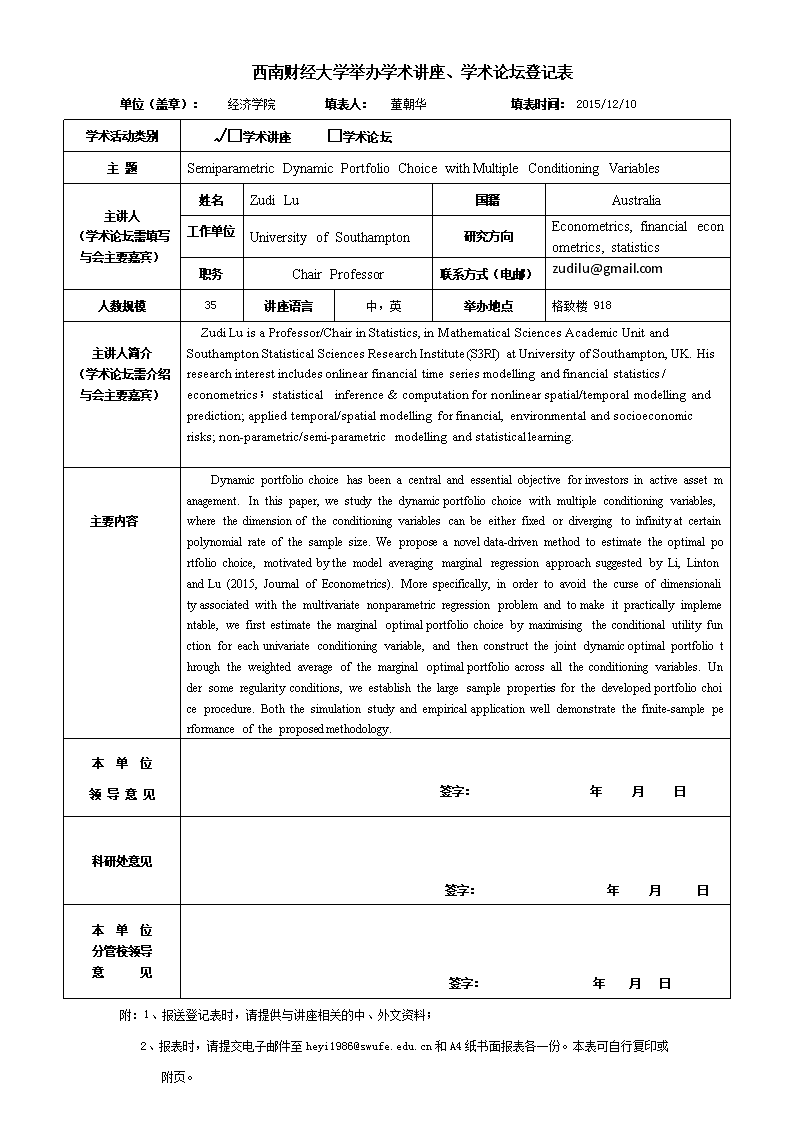

'西南财经大学举办学术讲座、学术论坛登记表单位(盖章): 经济学院 填表人:董朝华填表时间:2015/12/10学术活动类别√□学术讲座□学术论坛主题SemiparametricDynamicPortfolioChoicewith MultipleConditioningVariables主讲人(学术论坛需填写与会主要嘉宾)姓名ZudiLu国籍Australia工作单位UniversityofSouthampton研究方向Econometrics,financialeconometrics,statistics职务ChairProfessor联系方式(电邮)zudilu@gmail.com人数规模35讲座语言中,英举办地点格致楼918主讲人简介(学术论坛需介绍与会主要嘉宾)ZudiLuisaProfessor/ChairinStatistics,inMathematicalSciencesAcademicUnitandSouthamptonStatisticalSciencesResearchInstitute(S3RI)atUniversityofSouthampton,UK.Hisresearchinterestincludesonlinearfinancialtimeseriesmodellingandfinancialstatistics/econometrics;statisticalinference&computationfornonlinearspatial/temporalmodellingandprediction;appliedtemporal/spatialmodellingforfinancial,environmentalandsocioeconomicrisks;non-parametric/semi-parametricmodellingandstatisticallearning.·主要内容 Dynamicportfoliochoicehasbeenacentralandessentialobjectivefor investorsinactiveassetmanagement.Inthispaper,westudythedynamic portfoliochoicewithmultipleconditioningvariables,wherethedimension oftheconditioningvariablescanbeeitherfixedordivergingtoinfinity atcertainpolynomialrateofthesamplesize.Weproposeanovel data-drivenmethodtoestimatetheoptimalportfoliochoice,motivatedby themodelaveragingmarginalregressionapproachsuggestedbyLi,Lintonand Lu(2015,JournalofEconometrics).Morespecifically,inordertoavoidthecurseofdimensionality associatedwiththemultivariatenonparametricregressionproblemandto makeitpracticallyimplementable,wefirstestimatethemarginaloptimal portfoliochoicebymaximisingtheconditionalutilityfunctionforeach univariateconditioningvariable,andthenconstructthejointdynamic optimalportfoliothroughtheweightedaverageofthemarginaloptimal portfolioacrossalltheconditioningvariables.Undersomeregularity conditions,weestablishthelargesamplepropertiesforthedeveloped portfoliochoiceprocedure.Boththesimulationstudyandempirical applicationwelldemonstratethefinite-sampleperformanceoftheproposed methodology.本单位领导意见签字:年月日科研处意见签字:年月日本单位分管校领导意见签字:年月日附:1、报送登记表时,请提供与讲座相关的中、外文资料;2、报表时,请提交电子邮件至heyi1986@swufe.edu.cn和A4纸书面报表各一份。本表可自行复印或附页。'

您可能关注的文档

- 2018年报考中共西藏自治区委员会党校在职研究生登记表

- 机构电子签名认证证书业务登记表

- 佛山市南海区招考政府辅助工作人员报名登记表

- 南京地铁2018届校园招聘报名登记表

- 天津市建设工程质量监督登记表

- 2014年狮山镇政府工作人员招聘报名登记表

- 中国科学院昆明植物研究所应聘人员基本情况登记表

- 附件1:兰州新区校园招聘报名登记表

- 吉林大学2018年申请考核制博士研究生登记表、专家 …

- 重庆大学治安综合治理联络员登记表

- 印刷企业承接境外印刷品登记表

- 22012年度经济专业技术资格考试报名发证登记表

- 档案管理情况登记表(表1-1)

- 放假期间学生在校住宿登记表

- 公路动物卫生监督检查站清理核查登记表

- 湖南省机关事业单位工勤技能 级岗位培训登记表doc

- 经济管理学院教师基本情况登记表

- 山东大学护理学院博士后研究人员应聘登记表doc